Looking forward to 2013, China's electronic information manufacturing industry will continue to be affected by the global economic recession, and it will continue to operate at a low level in terms of production, exports, and investment. It will be particularly difficult for the task of changing from strong to tough. How can China's electronic information manufacturing industry solve the problem of stagnating social investment in the new generation of information technology? How to more effectively start the domestic market to adjust the industrial structure? How do we try our best to avoid the "dilemma" pressure caused by the objective shift of industries? In response to the above problems, we should adopt a new generation of information technology industry development fund to promote the establishment of a new generation of information technology application and demonstration industry bases, ministries and organizations to implement the information consumer market cultivation project, adhere to the implementation of information technology production and cooperation special projects, and enhance the resources Regional industrial cluster supporting capabilities and other countermeasures.

Looking forward to 2013, China's electronic information manufacturing industry will continue to be affected by the global economic recession, and it will continue to operate at a low level in terms of production, exports, and investment. It will be particularly difficult for the task of changing from strong to tough. How can China's electronic information manufacturing industry solve the problem of stagnating social investment in the new generation of information technology? How to more effectively start the domestic market to adjust the industrial structure? How do we try our best to avoid the "dilemma" pressure caused by the objective shift of industries? In response to the above problems, we should adopt a new generation of information technology industry development fund to promote the establishment of a new generation of information technology application and demonstration industry bases, ministries and organizations to implement the information consumer market cultivation project, adhere to the implementation of information technology production and cooperation special projects, and enhance the resources Regional industrial cluster supporting capabilities and other countermeasures. Next year situation: communication equipment industry "leader"

In 2013, the development of China's electronic information manufacturing industry was facing a severe situation. The world economy, which has been difficult to recover, and the increasingly prominent internal contradictions have made the level of industrial growth not optimistic, and are facing a stagnant social investment in the new generation of information technology. Lack of effective policies and measures to initiate domestic demand production, and the pressure for survival of SMEs due to industrial transfer.

(1) The struggling world economy still constrains the development of the industry. At present, the uncertainty in the world economy is still rising. The European economy has experienced a complete recession. Although the US economy is slowly recovering, it is facing a "fiscal cliff," and the Japanese treasury is about to bottom out and emerging. The rate of economic growth has generally slowed down. These factors will continue to slow down the growth of the world economy in the intertwined effects. According to the IMF's forecast, the global GDP growth rate in 2013 was only 3.6%. Although it was 0.3% higher than that in 2012, it was still lower than the levels in 2010 and 2011, with 1.5% in advanced economies and 5.6% in emerging economies. In particular, it is worth noting that 44% of emerging economies have experienced financial imbalances. If a new round of global economic crisis erupts, it will be difficult for them to once again play the “recovery engine†role of the 2008 international financial crisis. It will be even more difficult for the world economy to embark on a steady growth track.

The global economy, which is still in a recession cycle, has a major impact on the development of China's electronic information manufacturing industry, which is directly reflected in the continuous decline in the growth rate of exports and investment. Since 2012, the growth rate of industrial exports has been hovering around 5%. From January to September, it only accumulated 3.4% year-on-year, which is the lowest level except for the negative growth of exports in 2009 due to the impact of the international financial crisis; it is accompanied by the entire national economy. The actual use of foreign investment fell for 5 consecutive months, and the growth rate of industrial fixed asset investment continued to decline. From January to September, the project investment of over 5 million yuan accumulated a year-on-year increase of 7.1%, which was the lowest level in the past 10 years, including investment from Hong Kong, Macao, Taiwan and foreign companies. Both showed negative growth, which were 11.2% and 12.7% lower than the same period of last year. It is expected that the "double-low" growth trend of China's electronic information manufacturing industry exports and investment will continue until the end of 2012. The annual growth rate will be about 5%; and in the absence of a clear improvement in the global economic environment, exports and The annual growth rate of investment will not exceed 10%.

(II) The growth of industry scale will not be significantly higher than the level of 2012. Under the external shock of the global economic recession, China's electronic information manufacturing industry increasingly highlights that the existing cost advantage gradually fades, the domestic demand market is difficult to start in the short term, and the new growth point of the industry remains There are potential internal issues such as cultivating and weak industrial chain integration capabilities of key enterprises. Since September 2011, the growth rate of industrial scale has gradually slowed down, which has changed the trend of stable and rapid growth that lasted nearly 18 months since the effects of going out of the international financial crisis in March 2010. In particular, since 2012, the growth rate of industrial scale growth has suddenly increased. Compared with the past five years, it is only slightly better than the level of 2009 that was affected by the international financial crisis. The cumulative sales value of each month has only kept a year-on-year growth rate of 11%. Around May, it fell for 4 consecutive months from May to August. The lowest point fell below 10% and fell to 9.9%.

At present, the growth rate of industrial scale has shown signs of recovery, which rose to 10.4% in September, and the overall development trend of the national economy has improved since the third quarter. However, various factors constraining growth still exist. Insufficient start-ups of enterprises and negative output growth of some key products. For example, 10% to 15% of the companies in the electronic materials industry have completely shut down or closed down, 80% of polysilicon companies have restricted production, production shutdowns or bankruptcies; overall manufacturers have generally cut upstream orders, and the growth rate of electronic component production has dropped for the sixth consecutive month. In addition, the exchange rate of RMB against the United States dollar has risen 16 times since late October 2012, and the exchange rate hit a new high of nearly 18 years, reaching 6.23, and the appreciation is expected to have a relatively large negative impact on the export of enterprises. Under the constant pressure of internal and external pressure, it is expected that in 2012, the growth rate of China's electronic information manufacturing sales will not exceed 12%. If there is no definite market advantage or strong measures are introduced, the growth of the industry in 2013 will not be significantly higher than This level.

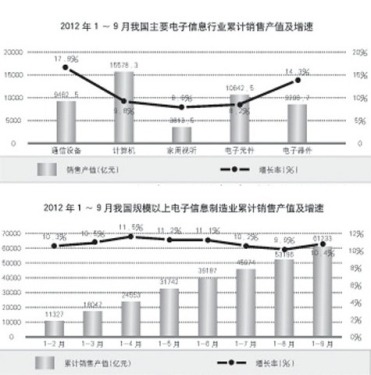

(III) Growth rate of communications equipment industry continues to lead The communication equipment industry in major industries continues to take the lead. As of September 2012, the growth rate of the communications equipment industry has been ranked first in China's electronic information manufacturing industry for 11 consecutive months. From January to September, the cumulative sales value increased by 17.9% year-on-year, which is higher than the industry average growth rate of 7.5 percentage points. In this regard, thanks to the strong growth in the demand for smart phone market, on the other hand, it is positively affected by the gradual warming up of global 4G (LTE) network deployment. It is expected that these two major favorable factors will play a further role in 2013, driving the communications equipment industry to achieve more than 20% growth throughout the year.

The growth rate of the computer industry is slightly lower than the average growth rate of the industry. The international market demand for PCs is shrinking. In the third quarter of 2012, global PC shipments have experienced the first decline in 11 years, a year-on-year decrease of 8.3%. This led to a year-on-year increase in the cumulative sales value of the computer industry in China from January to September of 9.8% year-on-year, which is lower than the industry average growth rate of 0.6%, which means that the growth pressure will continue to increase for quite some time in the future. However, China still has Lenovo, the world's largest computer maker in market share, and many foundries represented by Foxconn, and it also accounts for more than 80% of global tablet shipments. The considerable production scale will enable the computer industry to maintain a stable growth slightly lower than the average growth rate of the industry in 2013, and the annual growth rate is expected to be around 11%.

The growth rate of the home audio-visual equipment industry is relatively slow. Affected by the end of the home appliance replacement policy, the relative sluggishness of the domestic real estate market, and the spread of the “price war†in the international color TV market, the accumulated sales value of China's home audio-visual equipment industry only increased by 6.6% year-on-year from January to September 2012, which was lower than the industry. The average growth rate is 3.8 percentage points. With the in-depth implementation of energy-saving flat-panel TV subsidy policies and the accelerating popularity of smart TVs, the growth rate of the industry will rebound in 2013, but the international market capacity has stabilized, and the basic conditions for the early release of consumer demand in the domestic market will not change. The annual growth rate is expected to remain around 10%.

The growth rate of electronic devices and components industry is different. The cumulative sales value of the electronic device industry from January to September 2012 increased by 14.3% year-on-year, 3.9% higher than the average growth rate of the industry, mainly due to the cyclical rebound in the integrated circuit market, the steady increase in the export value of LCD panels, and the demand for electroacoustic devices. The driving force of continued growth is expected to continue to be effective in 2013, and the industry's annual growth rate will remain at around 16%. The cumulative sales value of the electronic components industry from January to September increased by 8.2% year-on-year, which was lower than the average growth rate of the industry by 2.2 percentage points. This is obviously constrained by the international economic environment. On the one hand, the export volume of other component products except optical cables is On the other hand, Japanese companies such as Panasonic, Sony, and Sharp have suffered huge losses, which greatly reduced the production and export of component production bases in China. It is expected that they will not be able to fundamentally improve in 2013, and the annual growth rate of the industry is still difficult to exceed 10%. .

(IV) The growth rate of the industries in the central and western regions shows a trend of rational decline The electronic information manufacturing industry in China is undergoing a trend of “from east to west and from south to northâ€. The growth rate of industrial scale in the central and western regions has increased dramatically, and the eastern region has experienced a significant increase. The high base, higher labor costs, and lower growth in resource and environmental capacity have caused a sharp contrast between low-speed growth and new regional growth poles. From 2008 to 2011, the sales growth rate of electronic information manufacturing enterprises above designated size in the central and western regions was higher than the national average by more than 10 percentage points for 4 consecutive years. In 2011, it exceeded the peak value of 42 and 53.2 percentage points respectively. Since 2012, the central and western regions have maintained rapid growth, but they have clearly shown a rational decline. From January to September, they respectively increased by 32.7% and 39% year-on-year, and decreased by 24.5 and 32.2 percentage points from the same period of 2011.

This mainly includes two reasons: First, the adjustment of the layout of the computer manufacturing giants and OEMs of Hewlett-Packard, Lenovo, Dell, Acer and Foxconn to the west has come to an end. Due to fluctuations in the international market, there is no plan to expand production capacity. The growth rate of regional industries has dropped normally. For example, the growth rates in Sichuan and Chongqing from January to September were 31.4% and 94.1%, respectively, which was 28.4 and 117.9 percentage points lower than the same period in 2011; the second was that the solar photovoltaic industry had entered the “shuffle†stage, coupled with Europe and the United States’ “double oppositionâ€. In the lawsuit, most enterprises basically stopped expanding their production capacity, and some of them showed a decline in the growth rate in the photovoltaic industry as the key area for development in the electronic information field. For example, the growth rates in Jiangxi and Xinjiang from January to September were 5.7% and 16.6%, respectively, which was 28.4 and 10.8 percentage points lower than the same period in 2011.

Objectively speaking, the former implies that the industrial pattern in the western region is basically stable, a complete industrial chain has been formed, and the transition from ultra-fast growth to rapid growth is bound to be conducive to the sustainable development of the industrial undertaking; the latter means that the overheated investment sector has gradually cooled down. The industry is moving out of disorderly competition through the market's "survival of the fittest," and the central and western regions will more cautiously choose the industries they have transferred to and increase the level of industrial acceptance. It is expected that in 2013, the central and western regions will maintain relatively rapid growth, and the growth rate of the industrial scale will be within 50% of the whole year; while the growth rate of the industrial scale in the eastern region will gradually pick up under the traction of the transformation and upgrading, and will remain at 10 for the whole year. %about.

Concern: The domestic market is weak

(I) Social investment in the new generation of information technology may enter a stage of stagnation. The new generation of information technology industry requires the government's financial resources to make substantial investments, but it also needs to attract a large amount of social capital to invest in sustainable development in a market-oriented environment. From the perspective of the flow of social capital in the last two to three years, China’s new generation of information technology industry has received a large amount of capital investment, especially in hot-spot areas such as solar photovoltaic cells. In 2011, the total investment exceeded RMB 150 billion, and the growth rate exceeded once. 110%. However, as the overall development environment of China's electronic information industry becomes increasingly severe, and the deep-seated problems of the industry itself have become increasingly prominent, it is possible that many areas of the new generation of information technology will face difficulties in attracting social funds in 2013.

First of all, there is a lack of hotspots that can generate large amounts of output in the short term. Many high-generation LCD panel production lines have been put into operation one after another. The solar photovoltaic industry has entered the “shuffle†stage. It is still some time before the LED market is fully started. With the exception of smartphones and smart TVs, the choice of social funds is not many, but for smart terminals. Most of the investment is concentrated in the assembly of the whole machine that cannot reflect the characteristics of the new generation of information technology. Second, there is still no reliable and mature business model. At present, there is not a large-scale IT company that can use cloud computing or related fields of the Internet of Things as its main source of income. Both rely more on national financial input, and lack of access to social funds for profit-oriented purposes. Finally, there is a lack of scientific planning and design for investment. The overheated investment in the solar photovoltaic industry and the LED industry has caused social capital to be vigilant. However, the fund allocation is completely dependent on the market-based mechanism, and it is difficult to form a macroscopic investment strategy for the new generation of information technology industry. At present, the country is not relevant in this respect. With planning and guidance, the future growth of the industry is not yet clear, and social capital will become more conservative as it enters, slowing investment growth.

(2) There is still a lack of effective policy measures to start the domestic demand market. Starting the domestic demand market as soon as possible is an inevitable way for China’s electronic information manufacturing industry to mitigate the impact of international market fluctuations, adjust the industrial structure, and ensure steady and rapid sustainable growth. For industries such as LED, which urgently need to expand the market space for application, it is of outstanding significance. However, China’s current domestic demand market for electronic information manufacturing has adopted a relatively simple policy approach. From household appliances to the countryside, household appliances to old-to-new energy-saving products and people-friendly projects are concentrated in the consumer market, and individual consumers are The main carrier for stimulating domestic demand.

This will create at least two problems. In 2013 it hindered the start-up and expansion of the domestic market. On the one hand, the policy of starting the domestic demand market is only for individual consumers, and will be limited by the level of consumer income and the possession of home electronic information products and the elimination rate. It is difficult to promote the export-dependent status of China's electronic information manufacturing industry for more than 55% for a long time. There is a substantial decrease in the degree. In addition, policies such as home appliances going to the countryside and home appliance trade-in programs have great potential for inducing market demand in advance and overdraw consumers' future consumption. The growth in domestic output value of the computer industry and home audio-visual equipment industry supported by the home appliance trade-in policy for the period from January to September in 2012 was lost. At the same time, they were reduced by 31.4 and 9.3% respectively compared with the same period in 2011, in which the domestic output value of the computer industry was negative growth (-2.0%). On the other hand, the policy will only focus on the important role that individual consumers will ignore in the producer market and the industrial application market in expanding domestic demand. The domestic demand of the producer market lies in the upstream and downstream self-supporting of the industrial chain. For instance, domestic production of domestic machines is more guided by the use of domestic chips; the domestic demand of the industry application market lies in the promotion of industry applications, such as the encouragement of equipment, industrial control, finance, power, and other important industries. More use of domestic electronic information products, systems and equipment. This is not only conducive to the expansion of domestic demand, but also conducive to China to create an autonomous and controllable industrial system.

(III) The objective trend of industrial transfer has gradually brought about the pressure of survival for SMEs The industrial transfer in the field of electronic information manufacturing industry is not fundamentally different from other types of manufacturing industry. The motive is that the various comparative advantages of the eastern region have gradually subsided. The premise is that the central and western regions have made major improvements in the areas of industrial systems, infrastructure, policy environment, financial logistics, and personnel reserves due to the economic and social development. This is not only a necessary way for China's industrial layout adjustment and optimization, but also an inevitable choice made by many companies to reduce operating costs, seize regional advantages, and obtain policy dividends, such as the transfer of production capacity from Foxconn to Chongqing and Zhengzhou, Henan. However, under the background of the current global economic recession, this “spontaneous†industrial transfer trend has brought about pressure on the survival of a considerable number of SMEs, and is particularly evident due to the accelerating pace of industrial transfer.

The Pearl River Delta and the Yangtze River Delta are the production bases of electronic components in China. About 80% of the electronic components companies are located here. With the significant increase in labor costs, the national minimum wage has increased by an average of 22.8%, and Shenzhen has reached 1,500 yuan/month. Some enterprises in the region have begun to transfer to Chongqing, Sichuan, Hubei, Jiangxi, and Anhui. However, the enterprises that can carry out the transfer have the characteristics of strong influence in the industry chain, close contact with the whole machine manufacturer, and prominent bargaining advantages. For most of the ordinary SMEs that do not have such characteristics, they do not face the transfer. The gradual loss of both cost advantages, which is often the only advantage of the company; and transfer means that away from the customer, the market and the supply chain, especially the size of the company itself is not sufficient to negotiate with the host government a lot of preferential policies. It is expected that in 2013, a considerable number of SMEs in the electronic information manufacturing industry in the region will be caught in a “dilemma†situation and even bankruptcy.

Countermeasures and Suggestions: Actively nurture the information consumer market (1) Promote the establishment of a new generation of information technology industry development fund to leverage the leverage and multiplier effect of government funds, guide the integration of private capital, and establish a new generation of information technology industry development fund. The fund will adopt the government guidance and market operation model, respect the laws of the market, learn from international and domestic successful industrial development fund management operation experience, and closely integrate major national strategic decisions such as the “Twelfth Five-Year Planâ€, focusing on the development of a new generation Information technology related companies. On the one hand, it closely cooperates with local related park bases, participates in regional investment funds, and guides the next-generation information technology industry in an orderly manner. On the other hand, it participates in social capital and guides it to enter a new generation of information technology in a scientific and orderly manner.

(II) Minor provinces have jointly built a new generation of information technology application demonstration industry bases to focus on the important growth points of next-generation information technology industries such as the Internet of Things, cloud computing, digital homes, next-generation mobile communications, and next-generation Internet, strengthening network operators. , vertical integration and integration of content providers, system integrators, product-based carriers, user experience-oriented, and specific operational models for the purpose of establishing a number of state-level provinces with distinctive characteristics, active innovation, and significant results A new generation of information technology application and demonstration industry base, with enterprises as the main body to achieve industrial scale effect and agglomeration effect, based on the company's independent survival and profitability based on the realization of business model innovation.

(III) Organize and implement the information consumer market cultivation project. Continue to implement energy-saving products to benefit the people and accelerate the introduction of semiconductor lighting, computers, servers, solar photovoltaic and other energy-saving products, implementation details and access measures. Relying on the development of smart grids to encourage the construction and application of large-scale photovoltaic grid-connected power stations, accelerating the promotion of solar PV on-grid tariff zoning and supporting sources of subsidies, and conducting off-grid applications and residual power of distributed photovoltaic power generation with fiscal subsidies, contract energy management, etc. On-grid pilots will promote the improvement of the technical system and management system that adapt to the characteristics of photovoltaic power generation. Accelerate the implementation of the Broadband China strategy, promote broadband network infrastructure upgrades, drive expansion of the information service market, and lead the upgrading of smart home appliances, mobile terminals and other electronic products with rich, diverse and interactive digital content, and constantly cultivate new consumer hot spots. . Combining education, medical, social security and other major informationization projects in the people's livelihood area, relying on the intelligentization of important infrastructure such as transportation, environmental protection, and water conservancy, support and guide the wide application of autonomous and controllable electronic information products.

(IV) Adhere to the implementation of special cooperation in the production and use of information technology Relying on the “multiplier planâ€, build pilot platforms in discrete and process industries, promote multi-domain and deep-level cooperation between information technology companies and industrial enterprises, and focus on promoting industrial control and machine tools. The R&D and industrialization of systems and products in the fields of electronics and automotive electronics have raised the self-sufficiency rate of information technology and products in the industrial sector. Organize and implement the "CNC Generation" equipment innovation project action plan, rely on backbone enterprises to build CNC technology development and promotion service platform, and promote the development and industrialization of NC technology through cooperation in production, research and cooperation, focusing on textile machinery, small and medium-sized machine tools and basic manufacturing equipment, In areas such as high-efficiency energy-saving products, we will carry out integrated innovations in numerical control technologies and products, develop numerical control technologies and product application demonstrations in areas with prominent industrial clustering effects, and join forces to jointly promote the construction of numerical control technologies and product specifications and standards.

(5) Concentrate resources to enhance the supporting capacity of regional industrial clusters Make full use of the “Twelfth Five-Year Plan†technology transformation special projects to support SMEs that are in line with the industry cluster's dominant development direction and supporting service capabilities to develop in the direction of “specialization and specializationâ€. Encourage large enterprises and small and medium-sized enterprises to improve professional cooperation and cooperation among enterprises through various methods such as professional division of labor, service outsourcing, and order production. Promoting the collaborative transformation of leading enterprises and supporting enterprises, supporting the technological transformation of the entire industrial chain of R&D, design, manufacturing, and marketing services, and promoting the development of industrial layout to industrial support, professional cooperation, intensive and efficient elements, and ecological environmental protection. Promote the establishment of new social organizations such as strategic alliances for industrial technology innovation, innovate cooperation mechanisms, strengthen collaboration among enterprises, enhance collaborative innovation capabilities, promote the formation of a close cooperation R&D system, and enhance the overall competitiveness of the industry.

With more than 15+ yrs rich MFG experience, you can definitely trust in and cooperate with.

Provide you with the supply of personal protective equipment. to help you safely get back to your daily routine.

Our products include pulse Oximeter Finger, Forehead Thermometer, Automatic foam soap dispenser, etc.

Our strict quality control protocol thoroughly vets every aspect of production, storage, and shipments all the way way to our end customers.

protective equipment, ppe personal protective equipment, definition of personal protective equipment

TOPNOTCH INTERNATIONAL GROUP LIMITED , https://www.micbluetooth.com